Business car finance lets your business acquire a car, ute, or van without paying the full amount upfront, while claiming tax deductions on interest, depreciation, and GST.

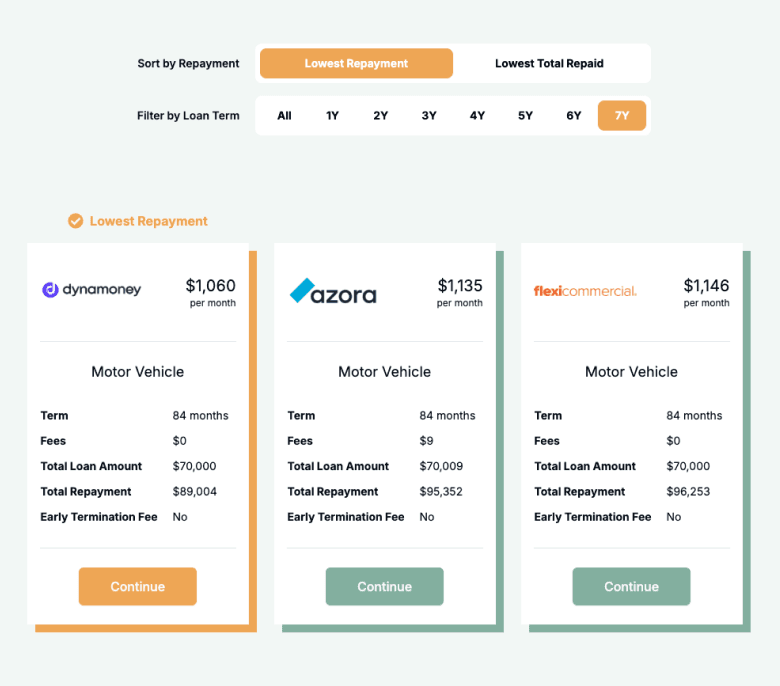

Rates start from 6.59% across Emu Money's panel of 50+ lenders, with terms from 1 to 7 years and loan amounts from $10,000 to $500,000+. The rate you're offered depends on your business turnover, time in business, credit profile, and the vehicle's age and value.

Four finance structures are available: chattel mortgage, hire purchase, finance lease, and operating lease. Each has different implications for ownership, tax, and cash flow. We compare all four in a single application, so you can choose the one that fits your situation.

For a closer look at current pricing, see our guide to business car loan rates in Australia.