Compare Machinery Finance Options from 50+ Australian Lenders

Access essential machinery and equipment without large upfront costs. Get personalised quotes in minutes with no impact on your credit score.

5.0 rating

Machinery Finance Made Simple

Finance new or used machinery with tailored options for Australian businesses. Preserve cash flow while upgrading equipment that drives efficiency and growth.

Borrow With Confidence

Amounts from $10,000 to several million

Flexible Terms

1 to 7 year loan terms available

Fast Approval

Funding often within 24–48 hours

Secured by Equipment

Lower rates when loans are backed by machinery

Industry Coverage

Construction, manufacturing, transport, healthcare and more

Tax Benefits

Potential deductions on interest and depreciation

How Machinery Finance Works

We connect you with lenders that specialise in machinery and equipment loans, so you can compare and apply with confidence.

Apply online in minutes

Enter details about your machinery purchase and business needs.

Get matched offers

Receive quotes from multiple lenders suited to your industry.

Choose your loan

Compare terms, rates and repayment options to select the best fit.

Get approved & funded

Approval and funding can occur within 24–48 hours.

Backed by over 50+ lenders

Giving you the best chance of being approved.

A quick guide to machinery finance

Machinery finance helps Australian businesses acquire essential equipment without tying up capital. Repayments are spread over time, freeing cash for staff, operations, or growth initiatives.

Loans are usually secured against the machinery, allowing lenders to offer competitive rates and larger borrowing limits. Terms typically range from 1 to 7 years, with flexibility in repayment frequency.

Finance covers a wide range of industries: construction firms can acquire cranes and excavators, manufacturers can upgrade CNC machines, logistics companies can expand vehicle fleets, and healthcare providers can fund diagnostic systems.

For businesses of all sizes, machinery finance provides access to modern, reliable equipment that supports productivity and growth without financial strain.

Want to skip ahead?

This guide is broken down into the following sections. Click a link if you want to skip ahead.

Types of machinery finance

Here are the most common machinery finance products available to Australian businesses:

Chattel Mortgage

A secured loan where you own the asset from day one while the lender holds a mortgage over it as security. Perfect for business equipment, vehicles, and machinery purchases.

Pros

- Immediate ownership of the asset

- Tax benefits - claim GST credits and depreciation

- Flexible repayment terms available

- Lower interest rates due to security

Cons

- Asset serves as security - risk of repossession

- Comprehensive insurance typically required

- Ongoing maintenance responsibilities

Best For

Established businesses looking to purchase equipment, vehicles, or machinery with immediate ownership and maximum tax benefits.

Finance Lease

A lease agreement where you use the asset throughout the lease term with the option to purchase it at the end. Ideal for businesses wanting to preserve cash flow while accessing essential equipment.

Pros

- Lower upfront costs and deposits

- Preserves working capital and credit lines

- Tax deductible lease payments

- Option to purchase at lease end

Cons

- No ownership until lease completion

- Total cost may be higher than outright purchase

- Early termination penalties may apply

Best For

Growing businesses that need equipment access without large capital outlay, or companies wanting to preserve cash flow for operations.

Hire Purchase

A financing arrangement where you hire the asset with an obligation to purchase it at the end of the term. Combines the benefits of gradual ownership with manageable monthly payments.

Pros

- Guaranteed ownership at term completion

- Fixed monthly payments for budgeting

- No large upfront capital required

- Tax benefits available during the term

Cons

- No ownership until final payment made

- Higher total cost than outright purchase

- Asset cannot be sold during the term

- Early termination may incur penalties

Best For

Businesses that want eventual ownership of assets but need to spread the cost over time, particularly suitable for essential equipment with long useful life.

What can I use machinery finance for?

Machinery finance can be applied across a wide range of industries and equipment needs:

Equipment Purchase

Buy new or used machinery essential for your business operations.

Upgrade or Replacement

Replace ageing machinery with modern, efficient models to boost productivity.

Expansion Projects

Acquire additional equipment to support business growth and new contracts.

Technology Investments

Invest in automation, robotics, or advanced manufacturing machinery.

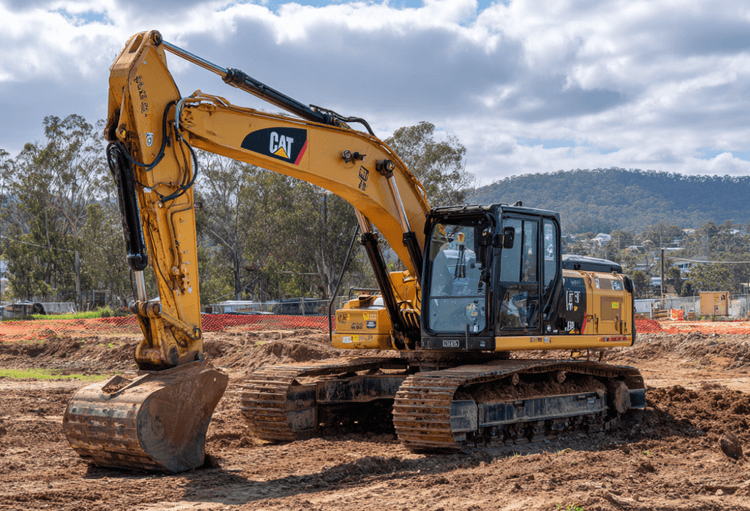

Construction Equipment

Fund excavators, cranes, bulldozers and other heavy machinery.

Manufacturing Equipment

Finance CNC machines, 3D printers, or full production lines.

Transportation Vehicles

Acquire trucks, vans, forklifts and other transport machinery.

Medical Equipment

Healthcare providers can finance diagnostic, imaging or surgical machines.

Agricultural Machinery

Fund tractors, harvesters, and irrigation systems for farming.

Hospitality Equipment

Purchase kitchen equipment, refrigeration, or large appliances for service businesses.

Case Study

Sanjay Patel, Brightside Constructions

Scaling a Construction Firm with Machinery Finance

Industry: Construction

Challenge: Unable to take on larger projects due to outdated and limited equipment.

Solution: A 5-year chattel mortgage secured against two new excavators and a crane.

Sanjay runs a mid-sized construction company in Queensland. He faced frequent downtime and lost contracts due to ageing equipment. Through Emu Money, he compared lenders and secured a 5-year chattel mortgage for new excavators and a crane. Repayments were structured to align with project cash flow. With modern machinery, the company improved efficiency, won larger contracts, and grew revenue significantly — while managing repayments predictably.

How much can I borrow with machinery finance?

Machinery finance in Australia typically ranges from $10,000 for smaller equipment to several million dollars for large-scale projects. The borrowing limit depends on machinery type, cost, age, and your business’s financial position.

Because the loan is usually secured against the equipment, lenders can offer higher borrowing limits and better rates than unsecured products.

Am I eligible for machinery finance?

Eligibility depends on the machinery type and your business’s financial health. Lenders assess turnover, bank statements, and repayment history before approving applications.

You may be eligible if you are:

An Australian citizen or permanent resident

Over 18 years old

Running a registered business

Able to provide recent bank statements

Hold an ABN (and GST registration if required)

How to apply for machinery finance

Apply online in minutes and get quotes from multiple lenders. Select your preferred option, upload documents, and funding is often arranged within 24–48 hours.

Documents you may need:

ABN and GST registration details

Photo ID (driver’s licence or passport)

Recent business bank statements

Tax returns or financials (for larger loans)

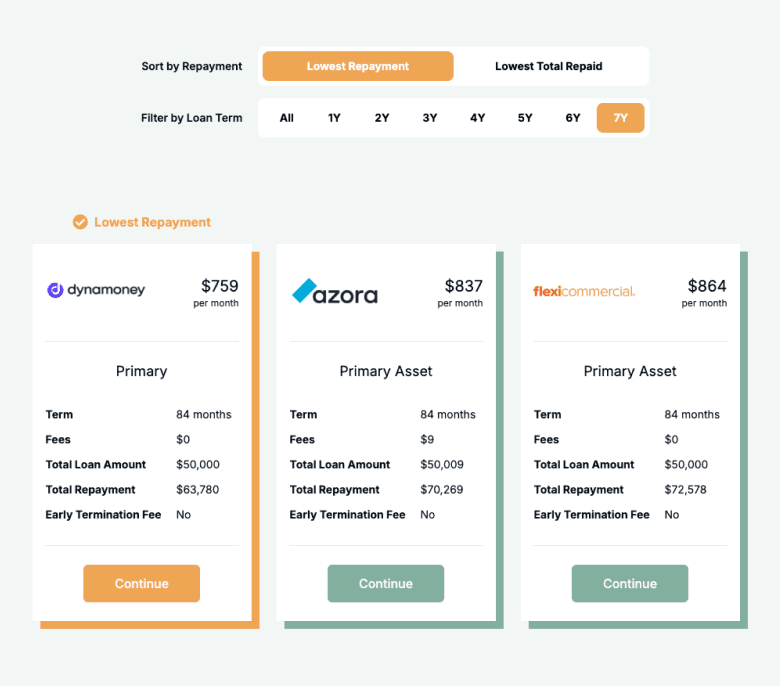

How to save money on machinery finance

To save on machinery finance, compare offers from multiple lenders. Shorter terms reduce interest but mean higher repayments, while longer terms ease cash flow but increase costs.

Check for establishment or early repayment fees that add to total expenses. If your business has strong revenue, making additional repayments can cut interest costs.

Align repayment schedules with your cash flow cycle to avoid late fees and financial stress.

Example: $250,000 financed at 7.95% p.a.:

| Term | Repayment Amount | Total Amount to Repay |

|---|---|---|

24 months | $11,281 | $270,744 |

36 months | $7,813 | $281,288 |

48 months | $6,125 | $294,000 |

60 months | $5,031 | $301,844 |

Understanding machinery finance options

Machinery finance products can differ in structure and cost. Here are key features to understand before applying:

Security: Asset-backed

Loans are usually secured against the machinery, lowering lender risk and improving rates.

Personal Guarantee

Some lenders require directors or owners to provide a personal guarantee for added security.

Term: Fixed vs Revolving

Most machinery loans are fixed-term, though revolving credit lines may be available for ongoing purchases.

Interest Structure

Fixed interest rates are common, providing repayment certainty. Variable rates are less common but possible.

Fees & Charges

Establishment fees, ongoing charges, and early termination costs can apply. Compare carefully.

Repayment Frequency

Repayments may be weekly, fortnightly or monthly. Align with your cash flow cycle for easier management.

Estimate your machinery finance repayments

See what your repayments would look like before you apply. Enter a loan amount, term, and rate to get an instant estimate with a full amortisation schedule.

- Compare finance structures

- Full amortisation schedule

- Instant results, no sign-up

- Adjustable rates and terms

Testimonials

See what our customers have to say about us.

![]() Verified Review

Verified Review

Brad was great from start to finish made the process very easy. Would have no hesitation in using emu money again. Thanks again Brad.

Toni B.

![]() Verified Review

Verified Review

Eujin was extremely easy to work with. He was respectful, clear in communication and persuasive. He works to get the best deal for his clients.

Chetan P.

![]() Verified Review

Verified Review

I applied for a car loan with the help of Emu Money a week ago, and the process was very fast and easy. There was no stress at all, as everything was taken care of by Krish, who managed my application from start to finish. He was very easy to communicate with and clearly explained the entire process and what was required from me. He was also quick to provide updates throughout. I would definitely recommend Emu Money to anyone looking for a smooth and hassle-free loan experience.. Thank you Krish.

Saritha A.

![]() Verified Review

Verified Review

Peter was very quick, responsive and easy to deal with. Great experience, and we're picking up our new car tomorrow!

Olivia F.

![]() Verified Review

Verified Review

I couldn't be happier with the service I received! Robyn made the whole car finance process so simple and stress free. She explained everything clearly, kept me updated the whole way through, and went above and beyond to find me the best deal. I honestly didn't think it would be this smooth, but she took care of all the hard work and I was in my new car before I knew it. Highly recommend to anyone looking for finance.

harry b.

![]() Verified Review

Verified Review

Emu Money does a really good job when it comes to their services. It was pretty easy and smooth, less stressful, quick, Cristal clear, very friendly, to the point...etc I would highly recommend them for anyone My agent was Eujin who made my dream come true with what I wanted achieved. Thanks heaps and all the very best. Regards Lankesh

Lankesh S.

Frequently Asked Questions

Machinery Finance FAQs

These helpful FAQs will help you find the answers you need. If you can't find what you're looking for, you can request a callback below.