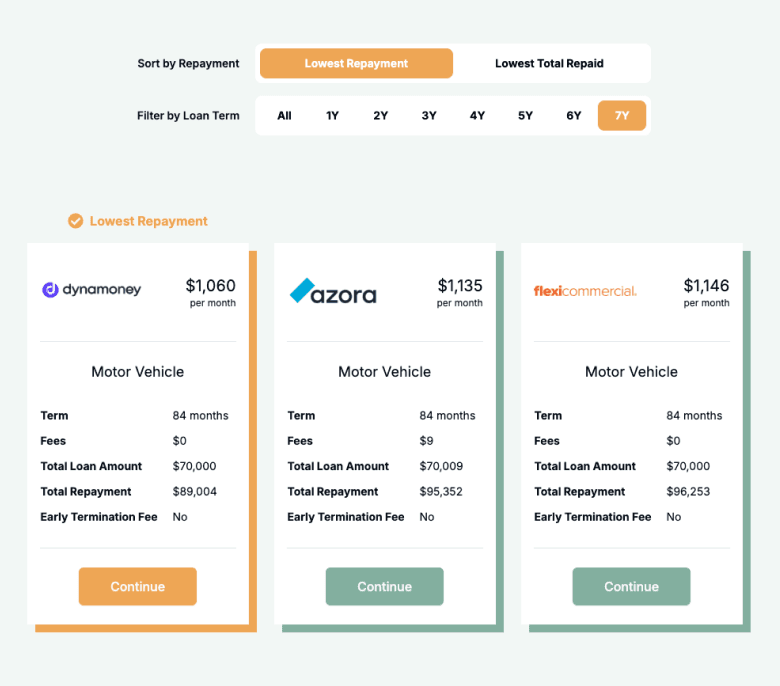

You can finance a new or used ute from $5,000 to $500,000 through Emu Money's panel of 50+ lenders. Rates start from 6.59% with terms from 1 to 7 years.

A mid-spec 4x4 dual cab costs $55,000 to $70,000 before on-road costs. Popular models like the Toyota HiLux SR5 4x4 ($63,990) and Ford Ranger XLT ($63,890) sit in this range. Financing over 5 years at 7% puts monthly repayments around $1,287 on a $65,000 ute.

Three finance structures are available: chattel mortgage (you own from day one), hire purchase (you own after the final payment), and finance lease (you lease with an option to purchase at the end). For most ABN holders buying a work ute, a chattel mortgage gives the simplest ownership and best tax position.

The key advantage of ute finance over buying outright: you keep your cash in the business while the ute generates revenue from day one. The GST credit, depreciation deductions, and interest write-offs can return a significant portion of the finance cost over the term. For a full breakdown of structures and how they work, see our guide to ute finance in Australia.