Compare Excavator Finance from 50+ Australian Lenders

Secure the excavators your projects demand without heavy upfront costs. Get personalised quotes in minutes with no impact on your credit score and keep cash flow steady.

5.0 rating

Excavator Finance Made Simple

Finance new or used excavators with structures tailored for Australian construction, civil, mining and landscaping businesses. Preserve working capital while upgrading capability and winning bigger jobs.

Borrow With Confidence

Typical amounts from $25,000 to $1m+

Flexible Terms

1 to 7 year loan terms available

Fast Approval

Funding often within 24–48 hours

Secured by Equipment

Lower rates with asset-backed lending

Seasonal / Project Fit

Match repayments to contract cash flow

Any Excavator Type

Mini, midi, crawler, long-reach, attachments

How Excavator Finance Works

We match your application to equipment lenders across Australia, so you can compare options and fund machines quickly.

Apply online in minutes

Share your business details and the excavator you’re purchasing.

Get matched offers

See quotes from multiple lenders specialising in heavy equipment.

Choose your structure

Compare rates, terms and balloon/residual options to suit cash flow.

Get approved & funded

Approval and settlement can happen within 24–48 hours.

Backed by over 50+ lenders

Giving you the best chance of being approved.

A quick guide to excavator finance

Excavator finance helps Australian contractors acquire critical earthmoving equipment without draining working capital. Rather than paying upfront, repayments are spread over time, keeping funds free for payroll, fuel, bonds, retention and bid pipeline costs.

Most facilities are secured against the excavator, which supports sharper pricing and higher borrowing limits than unsecured lending. Terms typically range from 1 to 7 years, with options to add a balloon or residual to reduce regular repayments. Repayments can be aligned to monthly cycles, seasonal slowdowns, or major project milestones.

Finance covers new and used units across brands and classes—mini/midi excavators for residential civil, through to heavy crawlers, long-reach and specialist machines for bulk earthworks, demolition and mining. Attachments such as buckets, breakers, augers and tilt-rotators can often be included.

The key is structuring the loan around your contract cadence and utilisation. With the right lender and terms, your excavator pays its way through productivity and billable hours, while predictable repayments support healthy cash flow and growth.

Want to skip ahead?

This guide is broken down into the following sections. Click a link if you want to skip ahead.

Types of excavator finance

The main products contractors compare when funding excavators in Australia:

Chattel Mortgage

A secured loan where you own the asset from day one while the lender holds a mortgage over it as security. Perfect for business equipment, vehicles, and machinery purchases.

Pros

- Immediate ownership of the asset

- Tax benefits - claim GST credits and depreciation

- Flexible repayment terms available

- Lower interest rates due to security

Cons

- Asset serves as security - risk of repossession

- Comprehensive insurance typically required

- Ongoing maintenance responsibilities

Best For

Established businesses looking to purchase equipment, vehicles, or machinery with immediate ownership and maximum tax benefits.

Hire Purchase

A financing arrangement where you hire the asset with an obligation to purchase it at the end of the term. Combines the benefits of gradual ownership with manageable monthly payments.

Pros

- Guaranteed ownership at term completion

- Fixed monthly payments for budgeting

- No large upfront capital required

- Tax benefits available during the term

Cons

- No ownership until final payment made

- Higher total cost than outright purchase

- Asset cannot be sold during the term

- Early termination may incur penalties

Best For

Businesses that want eventual ownership of assets but need to spread the cost over time, particularly suitable for essential equipment with long useful life.

Finance Lease

A lease agreement where you use the asset throughout the lease term with the option to purchase it at the end. Ideal for businesses wanting to preserve cash flow while accessing essential equipment.

Pros

- Lower upfront costs and deposits

- Preserves working capital and credit lines

- Tax deductible lease payments

- Option to purchase at lease end

Cons

- No ownership until lease completion

- Total cost may be higher than outright purchase

- Early termination penalties may apply

Best For

Growing businesses that need equipment access without large capital outlay, or companies wanting to preserve cash flow for operations.

What can I use excavator finance for?

Finance can cover machines, attachments and related project needs:

Construction & Civil

Fund machines for foundations, trenching, bulk earthworks and site prep.

Landscaping & Earthmoving

Acquire minis and attachments for tight sites, grading and drainage.

Road & Infrastructure

Scale fleets for roadworks, rail, utilities and government tenders.

Demolition

Finance high-reach units and breakers for safe, efficient demo works.

Utilities & Services

Trenching for water, sewer, comms and power installations.

Mining & Quarry

Heavy crawlers for overburden removal, loading and stockpiling.

Subdivision Works

Cut-to-fill, drainage, retaining and lot preparation.

Attachments & Transport

Include buckets, tilt-rotators, augers and sometimes delivery costs.

Case Study

Tane R., TRC Civil

Winning Bigger Civil Jobs with Excavator Finance

Industry: Civil Construction

Challenge: Missed tenders due to limited fleet capacity and rising maintenance on ageing machines.

Solution: A 5-year chattel mortgage with a 20% balloon on two new 14-tonne excavators and key attachments.

Tane owns a civil contracting business in Western Sydney. He regularly lost mid-size tenders because his single, ageing excavator couldn’t cover simultaneous sites. Through Emu Money, he compared lenders and secured a 5-year chattel mortgage for two new 14-tonne machines with quick-hitch, tilt bucket and rock breaker. The structure included a 20% balloon to keep monthly repayments down while utilisation ramped. Within three months, Tane won two council subdivision packages, improved uptime, and lifted revenue with predictable repayments matched to progress claims.

How much can I borrow with excavator finance?

In Australia, excavator finance typically ranges from $25,000 for late-model minis to $1m+ for heavy crawlers and specialist long-reach units. Borrowing limits depend on machine price, age, condition, expected life and your business profile.

Because loans are usually secured by the excavator, lenders can offer sharper pricing and higher limits than unsecured facilities, especially when utilisation and contract pipeline are strong.

Am I eligible for excavator finance?

Most construction, civil, mining and landscaping businesses qualify provided turnover and bank statements support affordability. Asset-backed security generally simplifies approval.

You may be eligible if you are:

An Australian citizen or permanent resident

Over 18 years old

Operating a registered business with ABN

Able to provide recent bank statements

GST registered (often required for larger amounts)

How to apply for excavator finance

Complete a quick online application to see quotes from multiple lenders. Choose your preferred structure, upload documents, and settlement can often be completed within 24–48 hours.

Documents you may need:

ABN and GST registration details

Photo ID (driver’s licence or passport)

Recent business bank statements

Asset quote/invoice and equipment details

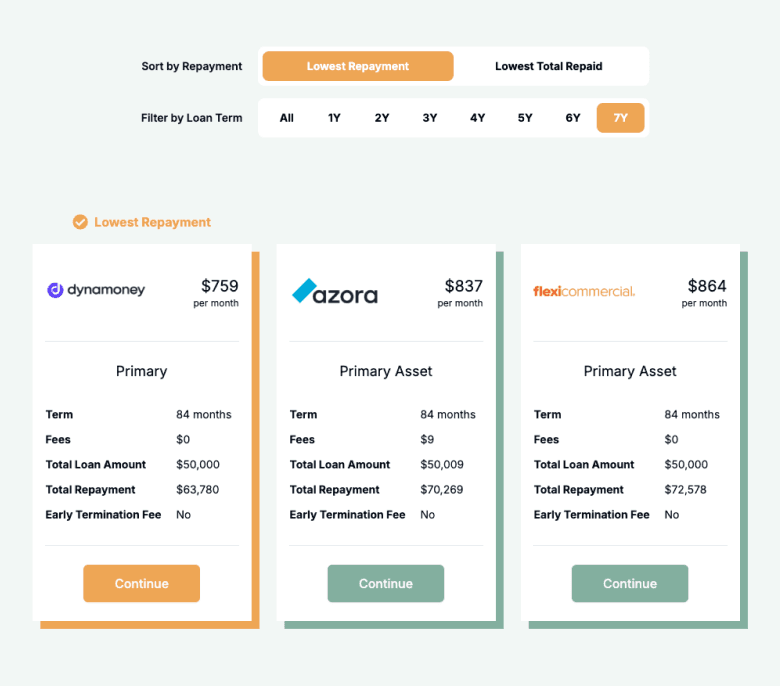

How to save money on excavator finance

Compare multiple lenders as rates and fees vary widely. A shorter term or smaller balloon reduces total interest, while longer terms or larger balloons ease monthly outgoings but increase overall cost.

Bundle attachments at settlement to secure sharper pricing and avoid future unsecured add-ons. Align repayment schedules with progress claims or milestone payments to reduce cash gap risk. Check for establishment, doc or early payout fees before you sign.

Example: $180,000 financed at 7.95% p.a.:

| Term | Repayment Amount | Total Amount to Repay |

|---|---|---|

24 months | $8,120 | $194,879 |

36 months | $5,618 | $202,242 |

48 months | $4,406 | $211,503 |

60 months | $3,623 | $217,402 |

Understanding excavator finance options

Know the structural levers before choosing a lender or product:

Security: Asset-backed

Most excavator finance products are secured against the machine itself. This reduces risk for the lender, allowing them to offer higher borrowing limits and more competitive interest rates. Unlike unsecured loans, the excavator serves as collateral, which can make approvals faster and terms more flexible for contractors.

Personal Guarantee

In addition to the excavator being used as security, many lenders also request a personal guarantee from company directors or business owners. This means you’re personally liable if the business defaults, reducing lender risk. It’s a common requirement across construction finance, so be sure you’re comfortable with the obligations.

Term & Balloon

Loan terms typically range from 1 to 7 years. Some lenders offer balloon or residual options, which reduce regular repayments by deferring part of the balance to the end of the term. This structure helps ease monthly cash flow, though it means a larger lump sum is due at maturity.

Interest Structure

Excavator finance is most often offered with fixed interest rates, giving contractors predictable repayments and stability over the loan term. Some lenders also provide variable rates, which may start lower but can increase with market conditions. Comparing interest structures ensures you choose the right balance between stability and flexibility.

Fees & Charges

Beyond the interest rate, lenders may apply establishment fees, documentation fees, account management costs, and early termination charges. These can vary significantly between providers, so it’s important to review the fine print. Factoring in all fees helps you understand the true cost of finance and avoid budget surprises.

Repayment Frequency

Repayment schedules can be tailored to suit your business’s cash flow. Options include weekly, fortnightly or monthly instalments. Some lenders even allow repayments to align with project progress payments or seasonal work cycles. Choosing the right frequency reduces financial strain and ensures repayments fit comfortably into your revenue cycle.

Estimate your excavator finance repayments

See what your repayments would look like before you apply. Enter a loan amount, term, and rate to get an instant estimate with a full amortisation schedule.

- Compare finance structures

- Full amortisation schedule

- Instant results, no sign-up

- Adjustable rates and terms

Testimonials

See what our customers have to say about us.

![]() Verified Review

Verified Review

Stevie was amazing she made the entire process smooth, not stressful and easy everything she requested wasn’t hard to complete, she worked around me she gave me advice or what to look for in a car she shared some good places to find a car she shared her experience with insurance she was amazing and went above and beyond. It isn’t always easy sharing things with someone when it comes to your personal affairs but she made me feel welcome to share you have a start worker and I really do believe she deserves a pay bonus

Tania W.

![]() Verified Review

Verified Review

Awesome to deal with. Brad was fantastic, nothing was too much trouble, handled all the hard work and let me get on with my business. Would totally recommend.

Charles L.

![]() Verified Review

Verified Review

Jackson helped me to get into a brand new car when no one else would consider me for a loan. Very happy with the service he provided.

jodie d.

![]() Verified Review

Verified Review

Dealing with Ryan has been excellent from start to finish ! Quick response no questions in answered great experience all round

Daniel W.

![]() Verified Review

Verified Review

Eujine made the process of getting a loan swift and easy, he's very trustable, I would highly recommend

Amila L.

![]() Verified Review

Verified Review

Received a wonderful, organised & professional experience with Evette. Recommend highly her service and knowledge.

Colin B.

Frequently Asked Questions

Excavator Finance FAQs

These helpful FAQs will help you find the answers you need. If you can't find what you're looking for, you can request a callback below.