You can borrow $5,000 to $500,000 with an active ABN in Australia, even without tax returns or a long trading history. ABN loans cover business loans, car finance, equipment finance, and lines of credit, all assessed primarily on your ABN status and business bank statements rather than traditional financials.

Most non-bank lenders approve within 24-72 hours using 3-6 months of bank statements. Banks typically require 2+ years of trading history and full financial statements, which rules out most newer ABN holders. Non-bank lenders fill that gap, accepting ABNs from 3 months old with consistent cash flow.

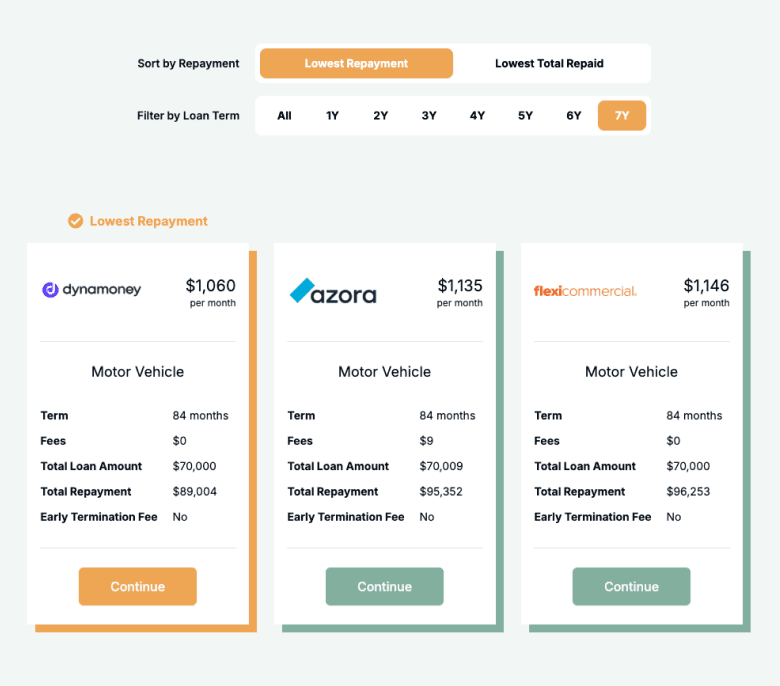

Rates start from 6% for secured ABN finance (where you provide an asset or property as security) and from 10% for unsecured products. For a complete breakdown of your options, see ABN Finance: Your Options Explained.