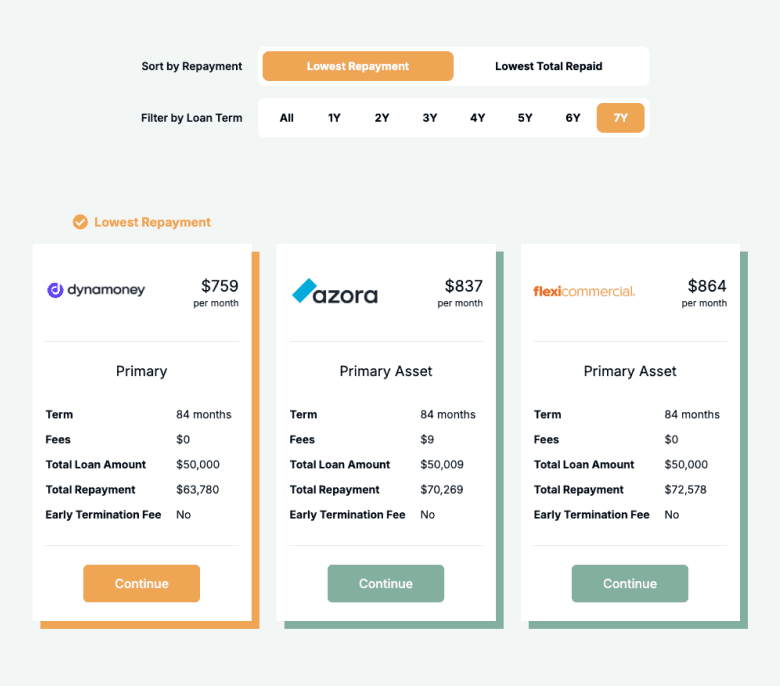

Asset finance lets you spread the cost of a business asset over 1 to 7 years, with rates from 6.59%. The asset itself serves as collateral for the loan, which is why rates are typically 3-7% lower than unsecured business lending.

The mechanic is straightforward: you find the asset you need, apply for finance, and the lender pays the vendor directly. You take delivery of the asset and make regular repayments over the agreed term. At the end, depending on your structure, you either own the asset outright or have the option to purchase it at a residual value.

Asset finance covers any tangible business asset with identifiable resale value. Vehicles, machinery, construction equipment, technology, medical equipment, hospitality fit-outs, agricultural machinery, and commercial solar systems are all eligible. The key requirement is that the asset must be identifiable (with a serial number or VIN) and have an established secondhand market.

On a $100,000 asset over 5 years, the difference between asset finance at 7% and an unsecured business loan at 14% is roughly $19,000 in total interest. That rate gap exists because the lender can repossess and sell the asset if you default, reducing their risk.