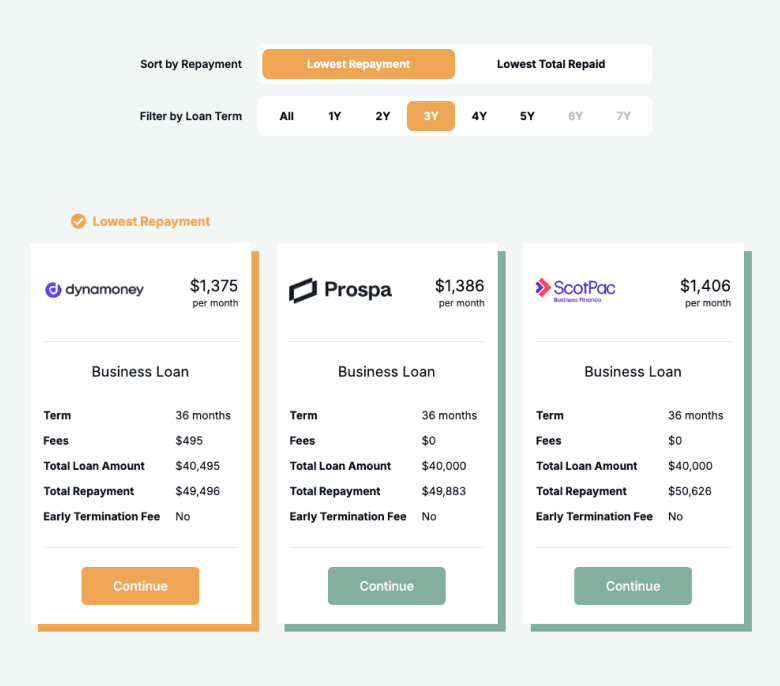

You can borrow from $2,000 to $2,000,000 with a business loan through Emu Money's panel of 50+ lenders. Rates start from 7.59%, with terms from 3 months to 5 years and repayments set weekly, fortnightly or monthly.

Business loans cover two broad categories: term loans (a lump sum repaid over a fixed period) and revolving facilities (overdrafts and lines of credit that let you draw funds as needed). Both are available secured against business assets or property, or unsecured based on your cash flow and credit profile.

The rate and amount you're offered depends on your business turnover, time trading, credit history, and whether you provide security. Secured loans typically attract lower rates because the lender's risk is reduced.

If you're financing a specific asset like a vehicle, equipment or machinery, a chattel mortgage, hire purchase or lease may offer sharper rates and better tax outcomes than a general business loan.